How Issuers React to New Market Dynamics

December 8, 2016

This Fall the municipal bond market has experienced a number of developments and emerging issues that may likely impact issuers in a very big way. We’ll get to some of the longer-term developments in subsequent posts, but the most important short-term development for bond issuers is the change in the yield-to-maturity curve and a completely new market environment.

Since the November presidential elections, a resulting rally in the stock market has contributed to an acute and violent sell-off in bonds. As is often the case, the sell-off in municipal bonds has exceeded that of Treasuries. Despite a stronger market this week in which bids seemed to stabilize, long-term rates were off (higher yields) by more than 80 basis points from November 8th to December 1st. What’s that mean to issuers? If the total volume in the bond market is between $350 billion and $400 billion, each basis point is worth between $350 million and $400 million in terms of higher interest costs for issuers (using some basic assumptions about yields and average life). Credit spreads are generally wider by 10-12 basis points today as well, and the slope of the curve has steepened by more than 50 basis points. According to Bloomberg, municipal bond funds experienced more than $5 billion in redemptions in the month of November. These redemptions, and the expectation for more going forward, will be priced in by big investors, which will continue to pressure rates for issuers selling bonds in 2017.

The key take-away for issuers is that the long-anticipated movement to higher rates is finally occurring. Most issuers have enjoyed access to very low-cost capital for a sustained period of time, with low rates and compressed credit spreads. That market may be now replaced with a more expensive bond market, a market in which investors have less cash and will be more selective when it comes to credit and bond structures. It’s incumbent on issuers, therefore, to adjust to the new normal.

This new market dynamic will require issuers to be much more proactive with their bond investors in two ways: first, issuers should have active dialogues with investors about their preferred bond structures in a rising interest rate environment. The ubiquitous 5% non-call 10 structure may fall out of favor. In fact, investors may prefer to invest on the shorter end of the curve and/or may prefer variable rate structures. Second, the delta in the pricing of new-issue bonds between issuers who are transparent and make their data easily accessible to bond investors, and those that don’t, will grow dramatically.

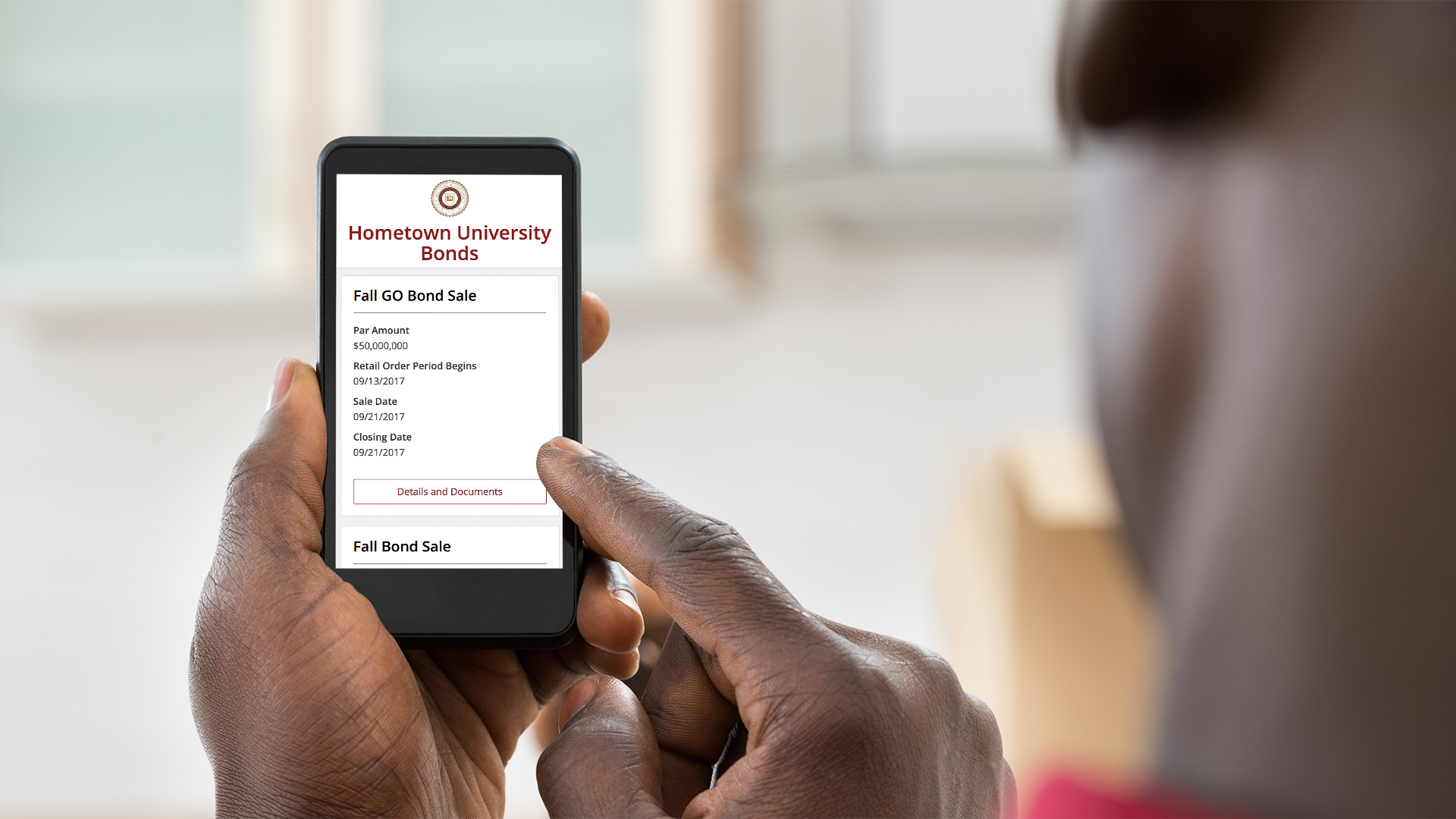

For more information on the BondLink investor platform, please request a demo here.

Colin MacNaught

CEO & Co-Founder @ BondLink